It's been a few days since I have posted anything, and it's

because I'm not sure what to say. There is so much happening: Russia/Ukraine, the NASDAQ dropping

massively and then rebounding, slope diminishing (when it should be

increasing), China and Taiwan tensions, the Omicron variant, political

division, and the list goes on. I'm not sure when I first heard the phrase:

"It's Easy Not To Be Wise," but I always reflect on it when I am heading to Las

Vegas, which we did this week for an in-person event. We were in person last week in Minneapolis

(-9 degrees!) and it was great to once again be in a room with other humans. I

have also been reflecting on this phrase over the past 10 days as I have seen so

much uncertainty in the marketplace.

Where does one start when faced with so many disparate

forces pulling at the markets? I try to take a measured view of what's going on,

and my conclusion is the title for this post. Trying to "be wise" right now is

a fool's errand. There have been many times in history that were probably far

more uncertain than this. Think about World War II and the invasion of Poland

the fall of Rome, Britain being bombed every night by the Germans, or the Civil

War here in the U.S. However, when you are amid struggles, it always seems that

the crisis is so intense that it's hard to be reflective. I thought this would

be a good chance to review the facts on the ground and try to get ourselves

centered, as we try to navigate through 2022. I'll do my best, but I'm sure

that I will miss some stuff, so please be patient.

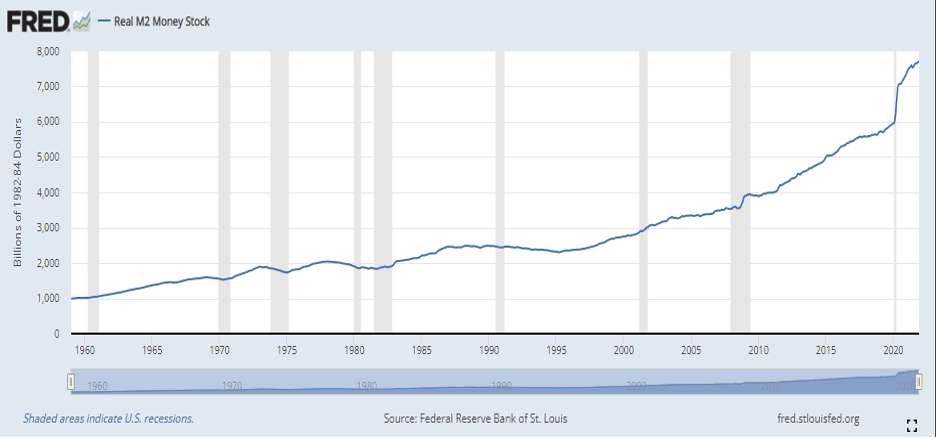

First, let us go to the four key fundamentals which I have reviewed many times over the past several years, namely: M x V = P x Q. Yes, they are boring, but so very important.

As you can see from the graph above, the money supply

continues to zoom higher. This should be a surprise to no one, given the

incredible spending that the government has been doing. However, according to

Mr. Powell, the pace of money supply growth should start to slow. We will see.

One way to take this into context is that in the last 10 years, the money

supply has roughly doubled. Ponder on that for a moment. That should be

massively inflationary…and indeed we do see inflation starting to pick up quite

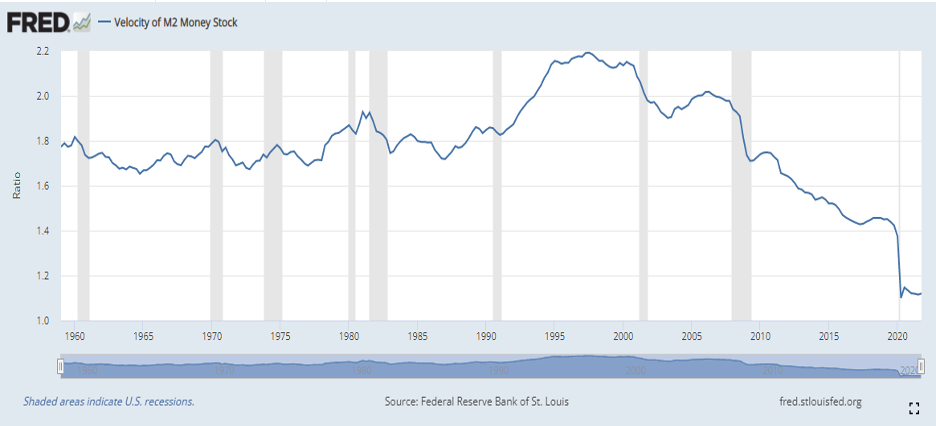

a bit. What about money supplies companion in the formula, velocity?

It appears that my old friend velocity has stabilized right

around 1.1-ish. I think this is a very important level because a drop below 1.0

would indicate deflation. But, if velocity starts to head higher quickly

in combination with the massive (inflationary) money supply we've already

noted, we could be in for a wicked bout of massively higher prices and rapid

inflation across the board.

So, one of the components of the equation is massively

higher and one is approximately unchanged.

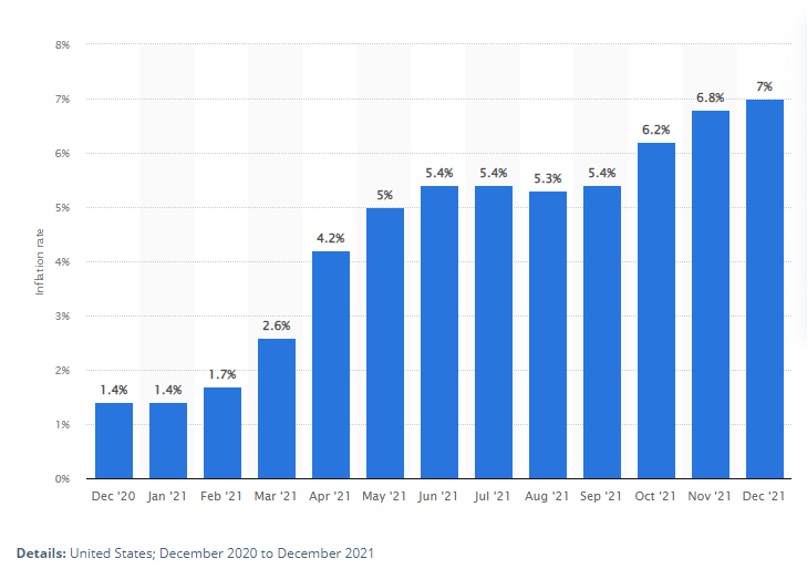

What about the other two components, prices and output? Well, clearly

prices are higher. Virtually every news

source has been commenting on rapidly rising prices around the country. You can see it in fuel prices, food

prices…pretty much everything. As you can see in this great graphic from

Statista detailing the monthly, 12-month inflation rate in the United States,

prices are accelerating higher.

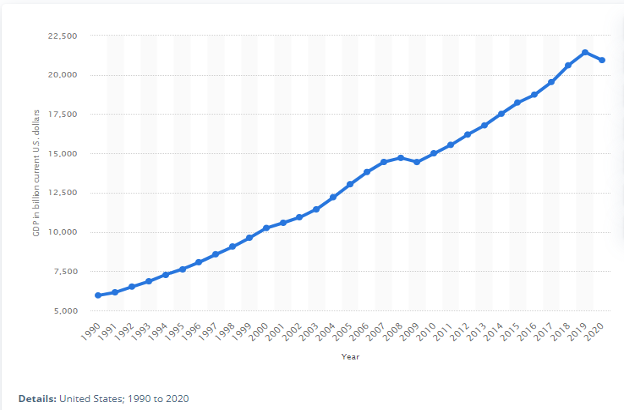

GDP is also heading higher, although it had a slight dip at

the end of last year. This is a good thing. Both sides of the equation must

balance, and we have seen the left-hand side is much higher lately. The only

way this all works without absurd price inflation is if GDP (Q in the equation)

can grow to fill up a good share of the right-hand side of the balance.

Right now, both factors on the right side of the equation

are heading higher. This tells us that the money supply has increased in order

to support good output growth, but that it has also contributed to price

increases.

What does it all mean? If I'm honest, I don't know. There

has been a lot of talk about the Fed taking away the punch bowl of monetary

stimulus. If that happens, and velocity remains low, then this would lead to an

imbalance in the fundamental equation—an imbalance that would correct itself,

one way or another.

One concept I learned a long time ago from the founder of

our firm Rich Berg, is the idea of open versus closed systems. In closed

systems like casinos and card games, there is a limited number of potential

outcomes. Most of these outcomes are known. For example, if you play Blackjack

at a casino, the "correct" play is known. If you turn certain cards and are

playing against a dealer, then you should do certain things. Books have been

written about this, and they sell little cards in the casino telling you what

you are supposed to do. The odds for every action can be calculated and you are

supposed to follow the book when making decisions.

In open systems, there are unfortunately no certain books we

can refer to. Open systems do not always have a best, knowable action.

Think about it: as you make portfolio decisions in your

institution, you are most likely not really considering the price of oil, or

even the direction of the stock market. You are looking at your balance sheet—and

your portfolio—and trying to make the best decision possible. Often this leans

on a lot of strong opinions about which way interest rates may be going.

And this is where I will try to tie my title back in: It's

Easy Not to Be Wise." Wisdom is a precious commodity, and this will be

paraphrased, but in the Bible (1 Kings 3), when God says to Solomon in a dream:

"Ask! What shall I give you?" Solomon's

famous reply is "wisdom and a discerning heart".

Pulling the famous King Solomon into a discussion is a

stretch, but boy could we all use some wisdom right now. How can one possibly

know what to do in such seemingly contentious times? What if Russia does decide to invade Ukraine? What if U.S. troops get involved? What about inflation?

The reality is that we do not know what will happen to the

stock market, interest rates, loan demand, deposits, the commercial real estate

landscape, the supply chain, politics, bitcoin, and on and on. So, since it is

so easy to not be wise, we just need to stick to the fundamentals of making

decisions based on the best math we can find, over time, contemplating a wide

variety of outcomes. You may be rolling your eyes at me right now because I

have said this so many times, but it's true. There are times when we should be

stretching for results and performance, and there are times when we should not.

Right now, feels like a time to try to stick to the fundamentals and not get

out over our collective skis.

I may be missing a massive theme or clear plan, and if I am,

please let me know! Clarity from the Fed and more "knowns" in the political

realm should help us out over the next 6-9 months, but in the meantime,

remember how easy it is to be unwise. Spend more time on analysis and

thoughtful research, and less time on high-risk gambits. There will be time for

that in the future.

Final, final thought: Speaking of how easy it is to be

unwise, I ate two hotdogs while watching that incredible Kansas City v.

Cincinnati AFC Championship Game. It seemed like a good idea at the time but

felt less wise later. But it certainly was a great football game!