The Chairman of the Fed is widely viewed as one of the most

influential and powerful people in the world of finance. When he speaks or

writes, people parse and explain every comment that he makes. Jerome Powell is the 16th chair of

the Federal Reserve and has held the position since February 2018. Perhaps none of his predecessors has seen a more

unbelievable time. He is known as a very collaborative and apolitical figure

and recently, was interviewed on 60 Minutes.

John Behof is someone I have worked with for over 20 years who

has been involved in many different parts of the banking industry, perhaps for

this topic, most relevantly as a regulator. John graciously offered to share

some of his thoughts on the recent Powell interview—he gave me a lot of new perspective;

I hope he does for you, too.

The FED Wants to Hold your Hand

The first record I ever bought was a song entitled "I Want

to Hold Your Hand," by the Beatles. It was a 45, which had one song on the

front and one song on the back. When I was watching 60 Minutes this past

week, this song came to mind. You may have noticed that Jerome Powell, the

Chairman of the Federal Reserve, went on 60 Minutes to explain the FED's

position on economic conditions. In addition, the Vice Chairman and other FED

governors scheduled speaking engagements over the days right after his 60

Minutes appearance aired. This seemed to me to be a coordinated effort to

get out the FED's "calming" message widely and strongly. And what was the

message? The message was that despite all the trillions of stimulus spending,

trillions of FED bond buying, very positive economic numbers, and direct evidence

of inflation, everything is under control.

The message was that any concerns that the FED (or the federal government)

should ease off the pedal to the metal approach to advancing the economic

recovery are misguided.

Watch the interview here.

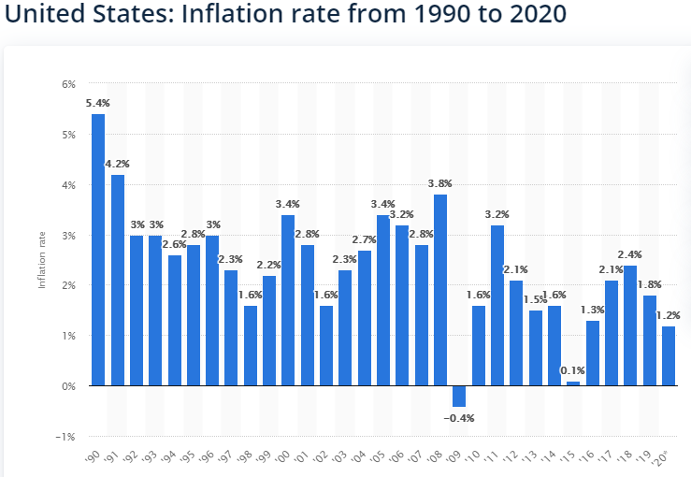

They said inflation is increasing but assured us that until

we hit an aggregate 3%, this is in fact a good thing. Inflation, they tell us, will

settle down when things get back to normal and: cheap goods are flowing again

from China, price competition returns, and productivity comes back. Their

message is that these increases in prices are "transitory" and will settle down

once we get back to normal. In addition, to get inflation to "average" 2%, which

they think is ideal, you have to let it run above 2% for a while. Their actual

fear is that once inflation does settle-down, it will settle down below 2%. It

appears that the FED's lesson from the last recession is that the prospect of a

long period of slow growth and deflation and disinflation should be much more

worrisome than too much growth and too much inflation.

You see, the FED is very concerned that the bond markets

have priced in an expectation of a not-so-transitory robust economic recovery

and inflation regime. The FED's own economic forecast went up dramatically from

January to March (their projections for GDP growth is now at 6.5% for 2021 and an

unemployment below 6%.) Despite the FED's best efforts to keep rates low, the

long-end of the Treasury curve sold off fairly dramatically between December

2020 and March 2021 (the 10-year went from 0.90% up to 1.75%; for now, it has settled

back to 1.55%.) The 30-year mortgage rate went from 2.68% to 3.08% over that same

period. The FED is unhappy that the markets, despite the FED's pontifications

to the contrary, are starting to price-in more inflation than the FED is

predicting and pricing in a stronger and quicker economic recovery than the FED

is predicting; this makes them unhappy because it leads to a buildup of the loud

and influential minority who are saying that rate hikes will come sooner than

the FED says they will.

So, the FED is unhappy with the return of the "bond

vigilantes," who are saying to the FED, more or less:

"We hear what you are saying, but we are seeing what we

are seeing, and your "pedal to the metal" actions may be too much for the economy

to bear. In the long run, you are on the verge of overheating this economy and

all the bad that comes with it."

So, what can the FED to do to calm the vigilantes, and get

those rates back in line? They are currently purchasing $120 billion of bonds

every month, which is historically huge, and have been doing so for over a year.

Increasing that activity could send out the wrong message, that maybe the

recovery is failing. They could shift some of their buying from the short end

to the long end of the curve, but the weakness in most of the short-end

auctions makes that strategy risky. A short-end sell-off could really make the

vigilantes more credible. The bottom line is that the bond investors on the

longer end of the curve are getting antsy and fearful and have been pushing

back by demanding more yield before they buy.

So, what is the FED to do? They can't buy more bonds; they can't shift their purchases. They can't stop the government spending. They can't stop the daily evidence that prices are increasing at a rate that appears to be higher than FED expectations. They can't stop the numerous economic releases that show the economic recovery is going very well, and may turn out to be much more robust than the FED is predicting. They can't stop the daily reports of how many people have been vaccinated and how ahead of schedule they are. So, what is the FED to do? How can the FED keep the pedal to the metal without allowing the bond vigilantes to push those long-term rates higher and higher?

Well, it appears the Fed has decided to try harder to get

their message out and make you believe it. The bond vigilantes can't get time

on 60 Minutes or give four speeches in one week, each with a hundred

reporters in the room to get their point of view out there. But the FED can.

The FED has decided that a public relations campaign will help them calm the

markets.

On 60 Minutes Powell said (again, I paraphrase):

Any observed excess inflation is temporary, and the FED

will let it run above 2% to get it to settle at 2%;

The economy is going well and the recovery is going well,

but is not in danger of over-heating—we have a long way to go to get back to

where we were;

The FED is being diligent about monitoring of the recovery

and stands prepared to do what is necessary to keep the recovery going, but is

carefully monitoring everything else; and

The FED knows the pedal is to the metal but won't let

anything bad happen. But the worst thing

it could do would be to react too diligently and quickly and get in the way of

a solid recovery.

In addition to Powell's handholding on 60 Minutes, the

next day FED Vice-Chair Richard Clarida gave a long speech echoing Powell's sentiment

in more technical terms. Additionally, other FED governors made comments, from

the same song sheet. So, the FED's answer to the fearful and antsy bond

vigilantes and the run-up in long rates is a communications blitz to convey that

the FED is on top of this recovery, is monitoring inflation closely, and does not

anticipate the need to take the pedal off the metal for a long time yet. They

are still on schedule and that there still will be no rate hikes until at least

2022 and very likely not until 2023. Nothing has changed in the FED's view,

even though many bond market participants were pricing in a lot more inflation

and a quicker recovery than the FED forecasts. Essentially, the FED's pundits

are saying, "How can the FED's response and actions at the height of the

pandemic be the same as now when we are nearly out of the woods?" Doesn't make

sense.

So, on April 15th, when a series of good economic data was released, including a pretty high inflation number, and the 10-year rallied from 1.62 to 1.55, many were surprised. It almost seems counter- intuitive. Those numbers would normally be bearish for bonds, but they weren't. It appears the FED's public relations campaign is working; its power to provide handholding and thereby calm the bond market by just talking widely, loudly, and publicly has been effective. It remains to be seen if the bond vigilantes have been temporarily sidetracked, have become believers, or are hiding in the bushes planning a new foray.

They used to say the "pen is mightier than the sword." In this day and age, that might be updated to say, "media exposure is mightier than the monetary toolbox."

I want to thank John for his insights—the next 12 months should

be very interesting. If you have specific questions for John, he can be reached

at jbehof@performancetrust.com.

Final, final thought: Every once in a great while, I feel a need to go to Taco Bell. It always tastes good, but it's also never a very good idea. It's kind of like selling cheap options…

Be sure to fill out the form below to subscribe to my weekly blog.