Back in mid-November, I wrote a piece called "A Dirty Word".

In that post, I discussed stagflation (the eleven-letter word) and said that it

was starting to sneak out of economists' mouths in dark corners and rarely

visited discussion groups. Today, it is being widely discussed and many openly

fear our slipping into the dark, dark world of stagflation. Is stagflation

becoming a reality, or is it just a scary talking point? Here is a link

to November's piece if you want to review.

To save you a little time and consternation, let me first review with you the definition of stagflation.

Stagflation is defined by three concurrent economic conditions—none of them good:

- Rising prices - a.k.a. inflation

- High unemployment

- A period of extended, slow economic growth

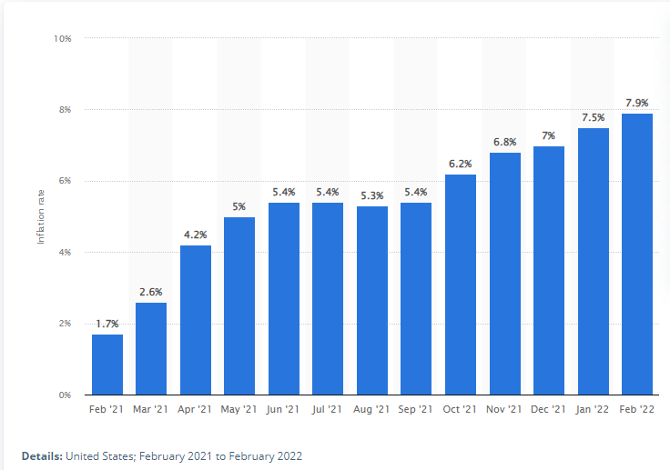

Let's start with inflation,

because unfortunately it is the easiest to identify and is most frequently in

the headlines today. Statista provides this stark graph.

Back when I wrote the November post, it was shocking to see the gas prices in California crossing the $5 per gallon barrier. Look at the difference just five short months can make to our perception of "normal".

Personally, the cost to fill my cars' tank has gone to and

sometimes beyond, $100. I think the local gas stations here in Illinois have

raised the max take for a pump from $75 to well over $100. For smaller cars in

the United States, the gas tank capacity can be around 12 gallons. For larger

cars, it is usually 15-16 gallons, and for many trucks, it can be around 20

gallons. Whether or not you want to blame this on the war in Ukraine or

political wrangling here in the U.S. it doesn't really matter. Gas, diesel

fuel, natural gas, and heating oil prices all have soared. The recent release

by President Biden of one million barrels of oil per day from the strategic

reserve is little more than a short-term band-aid.

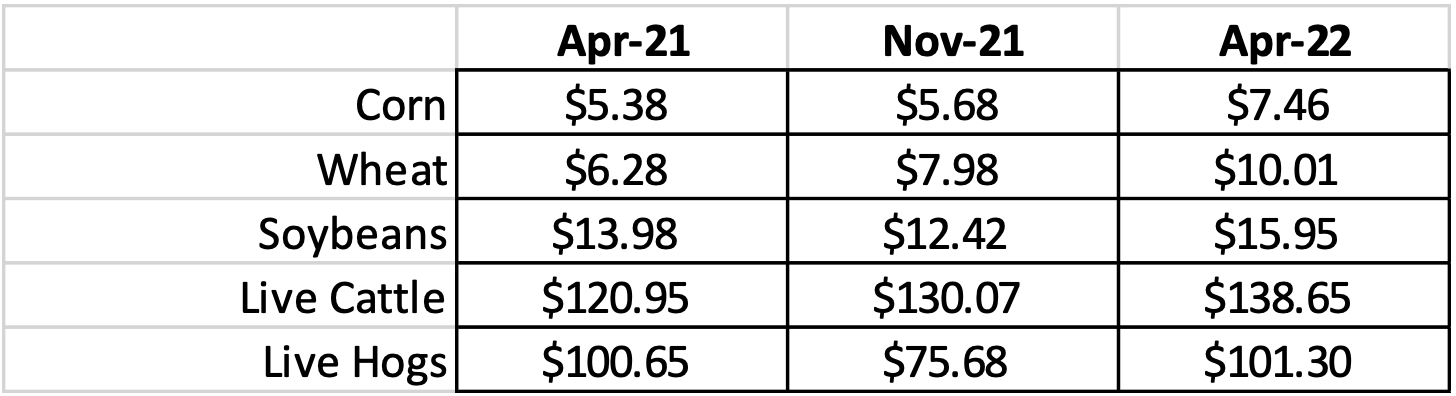

Now, let's very briefly discuss food costs. I quickly tabulated the raw cost of grains from last year to this year (source: Bloomberg - front-month futures). As has been widely reported in the news, Ukraine and Russia are both massive suppliers of grains, particularly wheat, and it should not surprise us that those prices are up. Of course, livestock need feed, and farmers need to power their equipment. Here is a brief sample of some of the prices of common agricultural products.

So, I think we won't have a huge argument about the

inflation part of this nasty little mix of conditions we call stagflation, but

what about the employment and output components?

High Unemployment

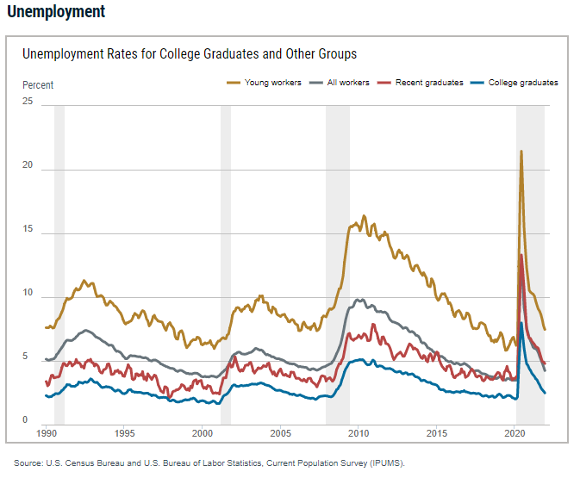

This is a real head-scratcher, because we have been through such a whirlwind in the past two years. According to the official data from the Federal Reserve Bank of New York, the unemployment rate in the United States has come down quite dramatically from the very scary highs at the start of the pandemic.

However, another stat from the same source would tell us

that on average, 42.5% of college graduates are currently described as

underemployed. The Federal Reserve Bank of New York defines underemployment as

"working in a job that typically does not require a bachelor's

degree". Recent college graduates are those aged 22 to 27 with a

bachelor's degree or higher. What does it really mean that so many college

graduates are underemployed? I think that is an important and lengthy

discussion. According to my research, this number is both a little fuzzier and

much less reported than the unemployment rate. It appears to me that historically,

around 20-25% of Americans are usually underemployed. It seems that we are

currently well above that number today.

So, the stats would tell us that the second part of

stagflation does not appear to be in place. In fact, it seems somewhat far off.

However, I think we can all see that the labor market is disturbed and rapidly

changing. I'm not quite sure what the massive shift from working in offices to

working in the home will eventually alter, but I do believe it will have

significant impacts going forward. Will it be a net positive or a net negative—I

think it's too early to tell. The next 12-36 months should tell a very

interesting story about the commercial real estate market. Everything from

shopping malls to office buildings, to downtown corridors will be affected. I

make sure to peek at the parking lot of the train station I commuted from for

20 years…it's still significantly below 50% full. If you start to think about

it, there is a new generation of employees that have never even been

asked to regularly work from an office. This must have an impact on the future

of business in lots of yet unidentified ways.

Extended, Slow Economic Growth

I'm going to start this section by referring to my favorite

economic formula: M x V = P x Q. As the Fed starts to play defense against the

rampant inflation discussed above, one of their key tools will be to slow the

growth of the money supply (M). We are already seeing this to some degree, but

you can bet that if inflation continues apace, the growth of the money supply

will slow. Velocity (V) remains historically low. We have already discussed

prices (P) via the examination of inflation, which leaves us with output,

a.k.a. GDP (Q). If the formula is correct, we currently have M still trending

slowly higher and V remaining very low. If the other side of the equation is

going to remain in balance, with P roaring higher, then Q cannot grow.

This is why the Fed must try to stop—or at least

dramatically slow—inflation. It must, and it will likely try to do so by raising

short-term rates. We have seen this process begin and we will likely see more

of it. I discussed this in my last post at some length.

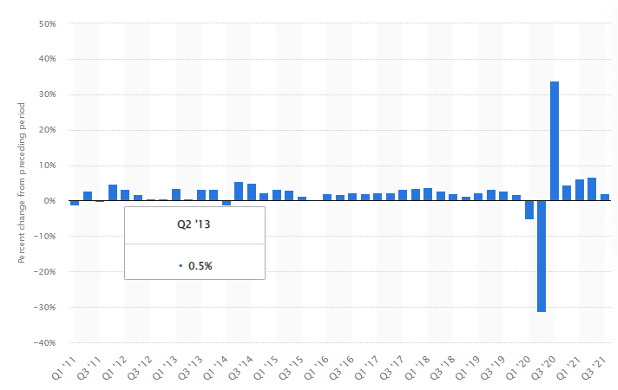

However, when we look at the current GDP (see graphic below from Statista), economic growth appears to be holding steady. I take the stats at face value, but I think we also must take the amazing shifts we saw during the pandemic into account. What will the medium-term effects be? Again, we don't know the future, but I believe it will be significant. Time will tell.

So, some good news: I think we can say that we have not

entered a period of stagflation…yet!

It is a rare and terrible cycle point that we need to avoid

at all costs. I do think that since I first covered the topic we have been staring

into that abyss for a while. Somewhere along the way, we could have easily

slipped into a terrible downward spiral, but so far, haven't. The war in

Ukraine obviously did not help. On a positive note, the airports have been

packed and the airline stats are looking pretty good over the spring break

period. People really want to return "to normal". If we do return to more

normal activity levels, perhaps we can leave this long and dirty word—stagflation—in

our rearview mirror!

Final, final thought: We are having a hard time breaking out

of winter here in Chicagoland, but grilling season is moving ever nearer.

Please send me some of your favorite recipes that can be enjoyed in the

sunshine.

Fill out the form below to subscribe to my weekly blog.