Almost exactly one year ago, I wrote a piece about Screwtape Proposes a Toast by C.S. Lewis. Here is how I introduced the work then, which should be a helpful refresh for this follow-up:

"C.S. Lewis is one of the greatest writers of the 20th century (at least in my opinion). He is famous for writing the Chronicles of Narnia, Mere Christianity, Surprised by Joy, The Great Divorce, and many, many others. One of his most popular works is a short book called The Screwtape Letters. The Letters were written by Lewis during World War II and apparently, he did not think they were very good. The basic theme of the book was that the senior tempter (Screwtape), a demon in the bureaucracy of Hell, was writing letters to his nephew (Wormwood) on how to tempt his "patient" and cause all kinds of trouble. Lewis covers many different areas of temptation in the book and Screwtape advises many tactics for exploiting human foibles and self-delusions. Unfortunately for Wormwood, he ultimately fails to destroy his human and claim his soul for the bad guys; the patient is killed and ultimately goes to Heaven, instead.

Screwtape Proposes a Toast that was written almost 20 years later for the Saturday Evening Post and takes on the form of an after-dinner speech given by Screwtape at the Tempter's Training College for young demons. Most people consider this book to be a critique of the American education system. Both books are wonderful reads and I hope you take the time someday to enjoy them..."

The quote from Screwtape's "toast" that I examined last

year, and would like to revisit now, is this:

"No man who says, 'I'm as good as you,' believes it. He would not say it if he did."

Last year, I was discussing how some of my worst meetings

over the last twenty-five years began with a portfolio manager telling me that he

or she didn't need any help because they already knew exactly what to do. As some

of you will recall, last year the 2-year Treasury was at 0.22% and the 5-year

was at 0.79%. We were just starting to come out of the pandemic-dominated

universe. Some states were still massively locked down - others were not. There

was very little loan demand, and I'm pretty sure that we were all confused and

confounded.

Today, I think I'm even more confused than I was then. Let's

review the short list.

First, the consumer price index (CPI), is expected to be

nearly 9%. It's outpacing the small wage gains people are experiencing. And

yet, the yield curve is inverting. If

the Fed raises the expected 75 basis points, will we see an even bigger curve inversion?

Who knows!

Second, the labor force is quitting. Only 62.2% of eligible

Americans are participating in our economy. I cannot imagine a scenario where

this is good. We also have a generation of new workers who don't know what it

means to "go into the office." Many of them are expecting (demanding) that they

have the freedom to work at home several days a week. Combine this with a

growing expectation for 3-4-day work weeks.

This cultural phenomenon would have been almost unimaginable just three

short years ago. In fact, as you will undoubtedly recall, way back in 2019, when

junior staff members wanted a work-at-home day, they had to have a good excuse.

The younger generation, more than anyone, was expected to be in early and stay

late to get their careers on a solid footing. My how the mindsets have changed!

Additionally, the Euro has gone from around $1.20 to roughly $1.00. Think about that. The last time that happened was nearly 20 years ago, in 2003. What does this mean for the capital markets? Also, consider that the yields on 10-year debt in the eurozone were mostly negative for a long time; today they are around 2%. Imagine the unrealized losses there must be on balance sheets holding long bonds bought at those negative yields.

Anything else? How about a massive leverage unwind in the

crypto space. What does it mean? This is

a trade that I have been confounded by for the last 3-4 years. I feel like I

missed it because I wasn't smart enough to fully understand it. I can't get my

head around things like this: there is an almost unexplainable token called

Polkadot (one of many!) that people are willing to exchange their hard-earned

money for. Here is how it is described in Bloomberg:

"Polkadot is a next-generation blockchain protocol that unites an entire network of purpose-built blockchains, allowing them to operate seamlessly together at scale. These application specific blockchains are called parachains and connect to the single base chain called the Relay chain. The Relay chain does not have any applications built on it but it contains Polkadot's consensus and other operational logics. DOT is the native token on Polkadot and is used to pay for transitions as well as to vote."

What does that even mean? How would one go about spending a Polkadot?

Bitcoin, the lead "coin" in crypto space, has fallen from $69,000 to $19,000.

If you entered the game too late, you have officially become what they call a weak

long. For those who employed leverage to play - yikes!

Christine

Lagarde, president of the European Central Bank (ECB), has warned that

cryptocurrencies are worthless and should be regulated. The ECB

boss believes that

regulating the sector will prevent people from gambling their life savings on

cryptocurrencies.

"My extremely modest opinion is that cryptocurrency is worthless. It is founded on nothing, and there are no underlying assets to serve as a safety anchor," she said. Lagarde continued, "I have always stated that these types of assets are highly speculative and extremely risky." Lagarde said on Dutch television that she is concerned about those who do not comprehend the risks, "who will lose everything," and who would be severely disappointed by digital assets.

(Source:

Bitcoinist)

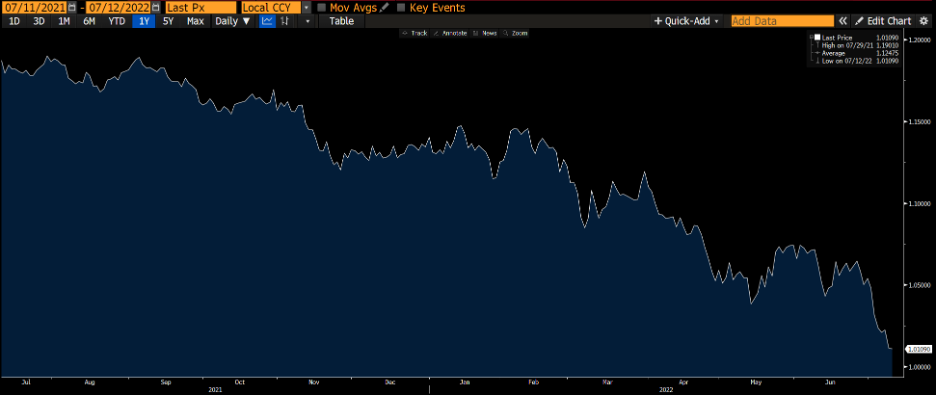

Here is the chart of bitcoin over the last three years. If I

slipped in a chart of the NASDAQ instead, it would look almost exactly the same.

How are crypto and exchange-traded stocks even connected?

That brings me back to the quote from the toast:

"No man who says, 'I'm as good as you,' believes it. He would not say it if he did."

As someone who sits and stares at his Bloomberg and

Interactive Brokers screens all day, I can tell you that I am less certain now than

almost ever before. I have my beliefs, as we all do. I believe that the stock

market still needs (more of) a massive wash out. I believe that an inverted yield curve is not

sustainable. I believe that we are headed for a semi-major recession. I believe

that we are in for a fairly major political swing. Etc., etc., etc.

How many of these beliefs are certain? 0%

The one truth I can keep going back to is that because we don't

know, so we must always keep an eye on multiple possible scenarios.

If we pretend to believe that we do know, then we are falling into

Screwtape's trap. As I get older, I realize that more and more often I need

advice from people who know more than I do. In many areas. This may sound a

little preachy, but right now is the time to seek advice, help, and analytics

from trustworthy sources. The capital markets, banking, and finance are all

changing in unpredictable ways.

Pretending to have all the answers is probably the one sure

way to fail.

By the way - I am starting a podcast next week!

In it, I'll be speaking with bankers and market experts from

around the country and following my own advice: reaching out to people who know

more than I do.

I hope you will join me on this journey. Links and

information to follow.

Final, final thought: I would love leads for great future

podcast guests. Please e-mail me at kfritz@performancetrust.com with your

suggestions on topics or anything else you think might help me get this new

endeavor up and running successfully.

Fill out the form below to subscribe to my weekly blog.

The information, analysis, guidance, and opinions expressed herein are for general and educational purposes only and are not intended to constitute legal, tax, securities, or investment advice or a recommended course of action in any given situation. Information obtained from third-party resources is believed to be reliable but not guaranteed. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. Past performance does not guarantee future results