Two years ago this week I started this little blog. So much

has changed, and yet so much has stayed the same. At the time, we were all

newly experiencing the pandemic. In fact, one of my two talking points in that

first post was the news that Moderna had just tested the very first COVID-19

vaccine. My exact observation was:

"The wires came out early in the morning with a report that Moderna (MRNA) a biotech company based in Cambridge, MA had successfully tested a vaccine in humans with no ill effect. The interview with the CEO Stephane Bancel was extremely positive: "This is a very good sign that we make an antibody that can stop the virus from replicating. The data couldn't have been better".

After this news, Moderna's stock jumped to an all-time high

of $87. The trials had begun with just a few hundred patients, and we were all

kind of freaking out. Spraying our groceries down with Lysol and living in a

weird dystopian world, was breakthrough news at the time. If my memory serves

correctly (always hard to confirm!) golf season was just beginning and many

courses were installing plastic barriers in the middle of most carts so COVID-19

could not be easily passed between players.

Further, rakes in the sand traps and flags on the greens were not to be

touched. Moderna's vaccine has turned out to be a winner, and the stock now

trades at just over $138 a share. We have learned so much. Sadly, the United

States just passed the one million mark for total deaths attributed to this

terrible virus.

My second major headline - in retrospect - was kind of unbelievable.

I talked about oil and discussed the market action that had recently taken oil

futures into negative territory for the first time in history. If only my wife would have let me store a few

thousand barrels of oil in the backyard! This was my commentary at the time:

"Oil has rallied significantly from the crazy negative prices experienced in late April when the front month contract traded into negative territory. This had, of course, never happened in the history of the oil market before. Part of the dislocation was due to the complete lack of available storage, so let's temporarily leave the "negative" prints out as a distortion - but still, spot and front month futures traded below $20 a barrel for nearly a month. I'm not an oil man, but it doesn't take a genius to figure out that no one makes money at that price (except possibly some storage facilities). As of this morning, the front month contract (which is June) is trading at $32.30. Still not at the average for the last year which is just over $49/barrel, but still a decent recovery."

Ah, if only we knew the future! I also did spend some time

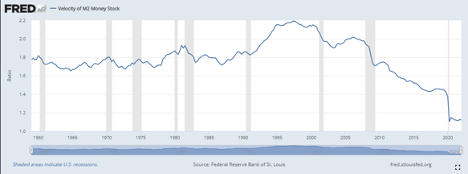

discussing the money supply and velocity of money and observed that velocity

was way down. Much of the decrease in velocity was due to the incredible

increase in the money supply. Readers of this blog know that I love to opine

about the M x V = P x Q equation. Some might say obsessively! Has the velocity increased

in the last two years? Actually, it has not. Here is the latest data from the

Fed.

What else has happened you may be asking? Well, we went into

and out of a recession. As you can see in the graph above where the lightly

shaded gray areas represent recessions, we went into official recession

territory in the second quarter of 2020 and then quickly started to recover

from the shocks caused by the pandemic. According to the numbers, we now sit

again on the edge of a recession and are also faced with an incredibly high

rate of inflation. The oil that I could have charged to accept into my backyard

way back in 2020 is now trading solidly above $100 barrel. The latest quote for

the front month contract as of May 17, 2022, was $114.50.

What a wild 2-year period.

One of the constants that I always consider when writing for

this blog is how little I actually know.

When I think of the future, it is so clear that we do not know what will

happen. Sometimes over the last two years, it has seemed a little like the

movie Groundhog Day starring Bill Murray.

This will date me a little bit, but that movie came out in

1993! If you know the plot, Bill Murray's character gets stuck in a loop where

the same day, February 2, gets repeated over and over, repeatedly. As you can imagine, this would be very

distressing. And for many of us, much of 2020 had that feeling. Many people had moved into their home

"office" and started doing the daily chores of the job. There were Zoom calls

and tons of e-mails, but very little personal interaction. Time kind of stood

still. From my office window, I watched the seasons change: the leaves fell,

the snow came, and spring sprung. And

2021 was almost, but not quite, a complete repeat. But now, finally, just as in

the movie, when Mr. Murray finally gets unstuck from his repetitive life,

things are really starting to change.

There is, however, at least one constant that will not change:

we still don't know the future.

One of the things that we always emphasize when teaching at

our Performance Trust University courses is that since we do not know for

certain what is going to happen to rates, slope, spreads, the economy or really

anything at all in the world of finance, we must do something that some might

consider mundane. It's a discipline of looking at multiple different scenarios,

over time, and projecting the potential outcomes to the best of our abilities.

By the way, this is almost impossible to do with stocks or any instrument with

unknown components. If you need proof of that just look at Twitter (sym: TWTR)! Who could have guessed just a couple of short

months ago the wild ride that Elon Musk was going to take it on?

Thankfully, we can have much greater clarity with fixed

income instruments. Certainly, even with these we can never be perfect, but as

we like to say, at least the system is somewhat closed. Elon Musk's tweets

won't change a bond's face amount. For example, I can know the cashflows of many

available bonds, such as when the coupons will be paid and when the principal

will be returned with maturity. For other

types of bonds, like mortgage-backed or asset-backed securities, the timing and

size of payments are far less certain, but they are still constrained by their

structures. But then, whether cashflow schedules are simple or complex, I still

don't know where interest rates will go while I am awaiting them.

So, what's the point? It does seem like we are breaking out

of this weird pandemic phase. I spend a lot of time researching and listening

to experts and I believe most of them feel we have started moving into what is

described as an endemic phase, where COVID-19 will regularly be found among us,

and we learn to live with it. Having recently flown for the first time without

mask mandates in two years, I can tell you that it felt great. Not having to

try and sneak sips of water with a mask on my face was incredibly liberating. I

don' think I will take that for granted for many years to come. But, for some,

there is still a lot of fear and discomfort in being around other people. That

may or may not ever change. I think there is a decent chance that a good

percentage of the population will be wearing masks for at least the next couple

years. Recently, we saw Shanghai, China

and North Korea impose incredibly severe lockdowns again. Could that happen

here? It seems unlikely, especially during an election season but I don't think

we can say it is impossible…can we?

I believe what we need to do is remain disciplined and get

very committed to a multi-scenario discipline to study our investments, our

loans, our deposits, and our capital. These things need to be examined and

understood in an extremely detailed way. The neat thing is that this belief of

mine has not changed over the past two years - or even the past twenty years!

Final, final thought: I

spoke in Dallas this week and have come to the sad realization that you just

can't get real barbecue up here in the north…but why not??!!

Fill out the form below to subscribe to my weekly blog.

The information, analysis, guidance, and opinions expressed herein

are for general and educational purposes only and are not intended to

constitute legal, tax, securities, or investment advice or a recommended course

of action in any given situation. Information obtained from third-party

resources are believed to be reliable but not guaranteed. All opinions and

views constitute our judgments as of the date of writing and are subject to

change at any time without notice. Past performance does not guarantee future

results