I watched a very interesting video recently contrasting the

behavior of cows and buffalos…I know, it sounds boring, but stay with me. In my formative years (0 - 9) I lived in northeastern

Nebraska and our house actually backed up to a pasture where cattle

grazed. They are not smart animals. In fact, the farmers use barbed wire to

establish boundaries for them and the cattle just never seemed to learn. If you walk into a barb-wired fence - it

hurts. But they would do it over and

over again. They are gentle and good-natured

animals, but smart? No!

We didn't see many buffalo in Nebraska, but if you keep

moving west across the plains and into Colorado you can come across huge herds

of them. They don't mess around. Buffalo are notoriously nearsighted, but they

have tremendous hearing and smell (meaning both what they put off, and what

they can sense!). They are not fearful animals

(like domesticated cattle); if they feel threatened, they will charge. In fact, buffalo are notorious for suddenly

turning on their pursuers and charging them.

If you have ever been on a wildlife tour or outing in the western

states, you'll recall that guides are very wary of the risk of a buffalo

suddenly charging. If they came across a

herd of beef cattle, they would have had a greatly reduced sense of

caution. That's why this four-minute video by Rory

Vaden really caught my attention

Let me summarize his talk. We know that storms come across

the U.S. from west to east. As they

cross the Rockies, cows can sense the storm - they hear the thunder, and sense

danger. They will begin moving east,

away from the storm, which continues to overtake them. Following an instinct to avoid danger, they

start to move away in fear. We know that

cattle cannot outrun a storm, and since they are moving in the same direction,

they exacerbate the impact. Eventually,

they are in the storm and moving in a direction to keep up with it longer.

To avoid trouble, they make things worse and end up spending even more time in

the wind, rain, or snow. They would have been better off just standing still

and letting the storm pass at its own speed.

Let's contrast this with buffalo. Buffalo exhibit a very different reaction to a coming storm. They will herd up, and run - not walk - into the approaching storm. How their species developed this instinct, I don't, know but think about how "smart" that is in its effect. By running at the storm, they add their speed to the relative passing speed of the storm, breaking through it that much sooner to the other side. Does this mean that the buffalo don't get wet, or snowed upon? Of course not. They still get soaked, but the duration of their storm affliction will be much shorter. Who knows if they even understand this as a "thought", be the result is they suffer less because they are taking it head-on and not trying to outrun something they can't.

You may be asking yourself, "What in the world does that

have to do with banking and finance?" Well, here are my inevitable tie-ins; we

all know that banking is facing a few different "storm fronts."

Fintech

Let's start with fintech.

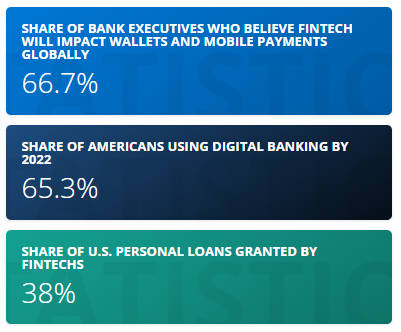

This graphic from Statista really caught my eye.

Think about that for a minute. Quite a strong trend. 65.3% (let's call it two-thirds) of all

Americans will be using some form of digital banking by the end of this

year. As of November of 2021, there were

10,755 fintech startups in the Americas, up from 5,685 in 2018. The storm clouds are gathering! The item that really shocked me was seeing

that 38% of all U.S. personal loans are being granted through some form of

online/electronic service. It's not just

the banking channel that Fintech is going after. They are involved in all kinds of services: money

transfers and payments, savings and investments, budgeting, financial planning,

and insurance, just to name a few. According

to a recent survey, roughly 75% of consumers globally have contact with one or

more of these fintech channels. In 2015

that number was just 8%. So, it's also a

fast-moving storm. I think as professionals

involved in the capital markets and in banking, we really need to ask ourselves

if we are trying to walk away from this storm, or are running into it. Whichever

we choose, we will get wet - the question is, which choice will result in less

overall discomfort? Fintech will change - has already changed -- banking and

the financial services industry for good.

Bitcoin/Digital Currencies

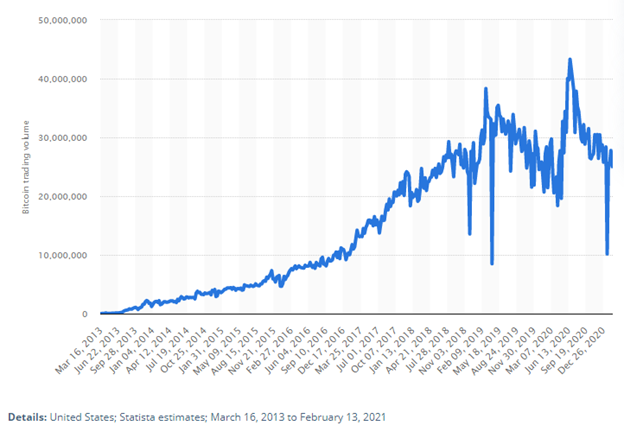

For 2020 it is estimated that there was roughly 1.5 billion dollars

worth of bitcoin traded. That's just

bitcoin. There are literally hundreds of

other "coins," and other digital assets being traded or exchanged all over the

place. Once again, Statista has come

through with a really great graphic showing the trading volume of bitcoin over

time, back to its beginning in March of 2013.

It has gone from near zero to around $30 million per week,

in just eight short years. It's global

and it's not going away. I must voice a mea

culpa on this one because I did not think it would last. I have to say that I acted like the cows, and

kind of tried to walk away from the incredible storm that digital currencies

have become. They have changed the way

transactions occur across the spectrum.

How has community banking reacted?

I still know for a fact that I need to learn more about how these

systems work and what they can do. Where

will I go to learn more about this? Probably not to my local community bank…but

what an opportunity that might suggest.

It's my belief that the VAST majority of people who are investing in the

"crypto" world have no real idea how it works or what it really is, in a

financial sense. They just see it as a

bright and shiny new trading vehicle, and many people "know" someone who found

untold riches by trading Bitcoin, Ethereum, Doge, or some other random digital currency.

Perhaps there is a community banking opportunity to educate

their customers about this new financial vehicle. I guarantee that some of the fintech's in the

previous section are busy doing just that, even if their business has nothing

to do with digital currencies, per se.

Inflation/Rising Rates

This is a storm that banks and credit unions may actually be

more instinctively prepared to embrace.

There is now very little doubt that inflation is here, and will be for a

while. All of the numbers released show

it, and anyone who purchases goods these days can attest to it. You've heard the chatter about the Fed and

rate hikes…25 - 50bps this time, and maybe several more to follow. If rates rise it will cause some emotional

pain in the short term - no doubt. As

the discount rate increases, it will be hard for many stocks to hold their prices. Fixed income portfolios will see declines in

market value for the first time in nearly a decade. But, as we head into this gathering storm, we

shouldn't forget that banks will make more money - overall - if rates

rise. This is a storm the industry

should want to "run into."

But it will get wet, windy, and cold, first. We must lead our institutions proactively. We need to get ahead of the curve and let our

stakeholders know what could be coming before it happens. Don't wait for the "red" numbers to show up in

an accounting report - run into the storm head-on, and let key people know

about the pain, and about the sunny skies that likely lie beyond. This will build credibility and confidence.

Will rates rise? We

don't know. It seems like they should,

but we are confined by the reality that we don't know the future. What happens if Russia invades Ukraine? There could be a flight to safety. The paramount task is to let people know what

might happen in various scenarios - not to get tunnel vision on only one

scenario. Or maybe I should say snow-blinded by one scenario. Embrace this uncertainty and use it as a

chance to demonstrate expertise.

Other storms

One thing we should also recall from our career experience is that unexpected storms may arise at any time. We don't want to be like cows - they aren't smart. Take storms head-on and rush into them. Will we get wet, and stormed upon? To be sure - we will. But what opportunities these can be to lead! Don't waste them.

Final, final thought: Watching the Winter Olympics is truly inspiring. Not only are you watching people achieve their lifetime goals, but you see so much support for each other across country lines.

Fill out the form below to

subscribe to my weekly blog.

The information, analysis, guidance, and opinions expressed

herein are for general and educational purposes only and are not intended to

constitute legal, tax, securities, or investment advice or a recommended course

of action in any given situation. Information obtained from third-party resources

are believed to be reliable but not guaranteed. All opinions and views

constitute our judgments as of the date of writing and are subject to change at

any time without notice. Past performance does not guarantee future results.