Most of us have had a little more time at home than we are used to these past several months. For me, this has given me the opportunity to watch some interesting movies (and I also continue to binge-watch Hell's Kitchen.) One movie I really enjoyed recently is called Greyhound, starring Tom Hanks as the commander of the Fletcher-class Destroyer USS Keeling. The Keeling's callsign for the purpose of radio communication is Greyhound. During World War II, there were huge convoys of supply ships going from the U.S. to Britain. Unfortunately, the technology of the time did not allow for effective air cover for the whole trip across the Atlantic, which left an area called the Mid-Atlantic gap (or more infamously known as the Black Pit). This area was where the German U-boats liked to hunt ships and earned the collective nickname of wolf packs (not to be confused with the positive use of that concept in other blog posts). The movie is fascinating because the technology of the day consisted of radio and light signals. The movie portrays Hank's character, Commander Ernest Krause, in his incredible effort to guide not only his ship but the entire convoy of 37 ships, across the Black Pit. Oh, how he could have used some modern anti-submarine technology, like helicopters and towed-array sonar.

Banking is currently in its own Black Pit. Some of the tools and technology we have used in the past are the equivalent of scratchy radios and flashing lights. The quote I referenced in a recent post was, "Life is like a ten-speed bike. Most of us have gears we never use."PT Score® is a new gear in the world of regulatory and risk management—our own towed-array sonar for hard-to-detect threats.

This week, I had the

opportunity to interview Bart Smith, the creator of PT Score, and I truly feel

he is the Greyhound captain who can help us navigate this hectic banking

environment and put this Black Pit in our distant wake.

Q: You have many unique insights into the risks that banks and credit

unions are facing this year. Can you summarize the two or three biggest

risks you see materializing in real-time?

The next biggest risk, in my view, is the potential impact on bank performance from a volatile interest rate environment. An extended period of low rates could eventually create unsustainable declines in real earnings for many institutions. Over the past 35 years, when financial institutions have faced economic or interest rate pressures, rates have declined and institutions have benefitted from increased asset valuations and reduced funding costs. In the current environment, there will be no funding relief from rates down, which means that increased income must come from higher yields on the asset side.As institutions pursue those yields, either through increased credit or duration, a new set of risks comes into play, particularly if rates reflectively begin to rise.

So…what is a bank or credit union supposed to do? In my opinion, this is a time where you must fully understand the broad risk exposures you carry as a company—not to curtail risk in a knee-jerk manner, but to establish a foundation from which to pursue unique risk/reward opportunities that could be beneficial to your institution during this particular time. This is not an environment where you can act on gut or past experience, or hide under the covers. Institutions need to more effectively leverage capital and optimize every income opportunity that is available. If you have a keen understanding of your risk position and you can articulate and support the basis for your decisions, you will be in a much better position to pursue reward strategies that could create huge advantages for your institution over the long-term.

Q: You talked about effectively leveraging capital and optimizing every income opportunity. Could you expand on that some more?

A: Yes…I believe

that the idea of effective leverage is one of the most misunderstood and misapplied

concepts in bank strategy. Institutions and their regulators tend to evaluate

capital levels based on past experience or the most recent rule of thumb. That

leads to capital trends that are not associated with an institution's

individual risk but are instead based on peer levels or concerns about

regulatory expectations. At the end of 2019, leverage capital ratios were at

historical peaks and were generally outsized in relation to the actual risk

undertaken by the industry.

Q: Over the past 4

years, your personal pet project PT Score has really come into its

own. Can you describe why you think it is such a critical tool for

managing risk in the industry? What are some of the latest innovations in

the tool that community-based institutions can use?

Institutions need to understand that there is no uniform regulatory position on strategies that are legally permissible. Regulatory viewpoints are primarily guided by the individual banker's ability to identify and manage the unique risks that exist within their own organizations. If you can effectively demonstrate a high level of proficiency with risk management, then you can pursue broader opportunities for performance without regulatory constraint.

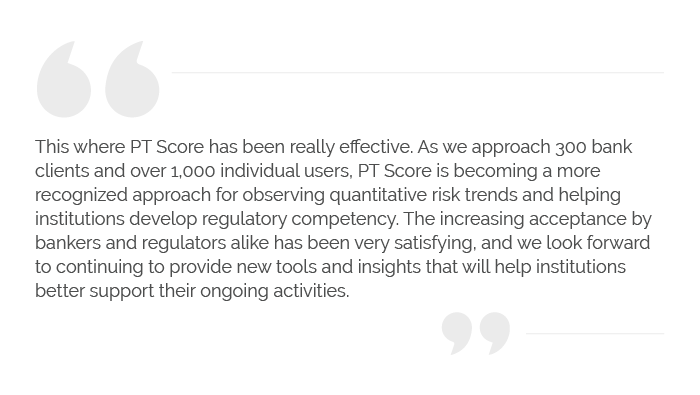

This is where PT Score has been really effective. As we approach 300 bank clients and over 1,000 individual users, PT Score is becoming a more recognized approach for observing quantitative risk trends and helping institutions develop regulatory competency. The increasing acceptance by bankers and regulators alike has been very satisfying, and we look forward to continuing to provide new tools and insights that will help institutions better support their ongoing activities.

In the early part of 2021, we have a number of exciting new enhancements that are scheduled for release including, but not limited to, a full scope enterprise risk management tool, increased interactive features for peers, and an entirely new version for credit unions. We are thrilled with everything that has occurred so far with PT Score, and we're looking forward to continuing to support our partners in the future.

I want to thank Bart for taking the time to answer my questions for all of us. One of the realities underlying the movie plot was that all the freighter captains were competent, experienced operators, but still, none of them would have been able to make it across the Atlantic without assistance from the Greyhound. In turbulent times, we can't let pride get in our way. Refusing to accept assistance in these situations can be downright foolhardy. Take protective action now. PT Score is just one of the tools available to you that quickly and dynamically show you the quantitative and regulatory impacts of potential decisions, giving you the conviction you need to act. Reach out to your Performance Trust contact to learn more.

Additionally, Bart has given me permission to invite you to reach out to him directly with your own concerns or questions. You can reach him at bsmith@performancetrust.com.

Final, final

thought: I made some killer mac and cheese with apples and chicken sausage.

E-mail me if you want the recipe—you will not be disappointed.

Be sure to fill out the form below to subscribe to my weekly blog.