I'm not sure how I came across this clip of Al Pacino giving a locker room speech…it's from a movie released in 1999 called Any Given Sunday but it caught my attention. It made me think of today's banking environment, and of this Rudyard Kipling quote I used in a post a year ago:

"NOW this is the Law of the Jungle - as old and as true as the sky;

And the Wolf that shall keep it may prosper, but the Wolf that shall break it must die.

As the creeper that

girdles the tree-trunk, the law runneth forward and back-

For the strength of

the Pack is the Wolf, and the strength of the Wolf is the Pack."

Banking and fixed income investing are both in a battle

right now—the same battle. Unprecedented.

Rates have never been this low for this long, and we need to be fighting

for every single inch we can get. Please

watch this clip—it is

R rated (or at least PG-13 as there is some foul language) -to get

inspired. We need to fight. There are no

easy wins right now.

For community banking to win and thrive, every inch of the

battlefield needs to be fought for—tooth and nail. The big boys have advantages

that we simply cannot match: technology, government support, and media. The

list goes on and on, and you know it better than I do. We—community based

financial institutions—need to fight. We need to fight hard, and we need to use

each other's strengths to survive. The time for trying to kill the competition

is not now. As Pacino says, we need to claw without fingernails for those six

inches that let us come out on top. I really think this means that we need to

support other as peer institutions across the country.

Having said that, I think portfolio management has also become a fight.

For the last couple weeks, I have commented on somewhat prosaic

topics, but today I want to talk about clawing with your fingernails for every

inch. For every basis point of return—not necessarily yield—and for every

possible advantage. This is no time to relax,

whether you are managing a portfolio of equities, fixed income securities, or

some combination of both.

This morning, as I rolled up to my computer to start typing

with the news stream playing in the background, I heard that some states are

going to reinstitute mask mandates. Without taking a political position, this

is extremely damaging to the psyche of the markets. I further noted that the

long bond had rallied over two points, taking the yield of the 30-year treasury

down to 1.83 and the 10-year note down to 1.20. This is not a healthy

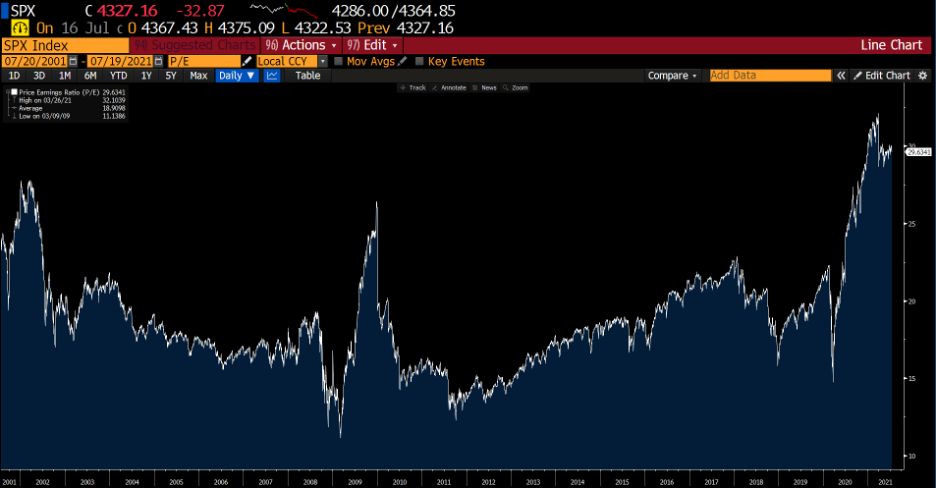

situation. With P/Es as elevated as they are—currently the P/E of the S&P

500 is around 29.6, near its 20-year high—and with so much money chasing assets,

it feels chaotic. Here is a graph of the P/E ratio for the S&P 500 over the

past 20 years.

Spreads on all risk assets have gotten tighter and tighter

all year. The imbedded options that banks and credit unions around the country are

selling, whether they understand this or not, are paying tinier and tinier premiums.

People are sitting on so much cash—effectively a non-accrual asset—that

decisions are being made we would normally never make. I have talked at some

length in the past year about SPACs, which are perfect examples of this

phenomena. We are starting to see the fruits of some of these imprudent decisions.

If the mask mandates and restrictions return broadly across

the country, the markets will not take it well. That is a non-political observation,

but a market-assessing one. In my opinion, it will not be good.

I like to play poker, and I have heard a particular phrase

get tossed around a lot: "The weak hands need to get flushed out." What this means

to me is that those "players" in this great game we call the capital markets—those

who have gotten in late, or who have chased yield by selling far too much

option risk for trivial premiums—will be forced out. It sounds cruel, but the

market will punish bad decisions at some point. If the rally in Treasuries

continues, options will be exercised, and bondholders (and lenders) will be

forced into lower and lower rates. If the P/E ratio noted above returns to

normal, people who entered late will be forced to sell—at losses. As they used to say when I was trading

futures, "The margin clerks will be sharpening their pencils."

So, what does all this have to do with Al Pacino and that inspiring locker room speech?

I believe that as people who manage money, you need to be

fighting for every single proverbial inch.

That means that sometimes we need to make tough decisions. Unpopular

decisions. It may mean that we need to do things that traditionally we have, or

have not, done.

I believe that as people who manage money, you need to be fighting for every single proverbial inch. That means that sometimes we need to make tough decisions. Unpopular decisions. It may mean that we need to do things that traditionally we have, or have not, done.

Hopefully, I will be dead wrong, and the market will hold firm

or slowly wind down, and my doom and gloom will turn out to have been unwarranted.

However, as you already know, the time to make corrections and adjustments is

not when the storm is raging. The time to make corrective preparations is while

the sun is still shining.

Final, final thought: The fluffernutter sandwich is

underrated. It's just tough to beat the combo of marshmallow and peanut butter.

Toasted.

Be sure to fill out the form below to subscribe to my weekly blog.