Followers of this blog know that food is important to me.

However, if I gave a quiz about the number of types of pasta, most of the readers

would probably not even be in the ballpark—I wasn't! According to Google, there

are upwards of 350 different types of pasta out there. Long, short, skinny,

thick, stuff-able, useful for soups, useful for lasagna, etc. If you have been

on a grocery shopping trip, you may have been assigned the task of finding a

specific type of pasta. The last time I went grocery shopping, I took note that

there were at least five different types (not brands) of spaghetti

noodles alone! incredible. I think we can all also agree that homemade noodles

are superior to store-bought noodles. There is something really satisfying

about making homemade pasta if you've never tried it, I highly recommend it:

fun and delicious.

I have often talked with portfolio managers about their

portfolios, describing it as a messy bowl of mixed-up spaghetti. There are all sorts

of different securities: treasuries, agencies, mortgage-backed securities,

CMOs, municipal bonds, and a variety of asset-backed securities. Bankers also

contend with tons of regulations, investment policies, and board preferences. Managers

outside banking can additionally throw in additional choices such as stocks,

corporate debt, futures, derivatives, private investments, and an almost

endless list of other potential "noodle" types that could be in the "bowl."

When I get sent to the grocery store to buy some pasta, I am

given very specific directions as to the type and size of noodles I am to bring

home. If spaghetti is on the menu for the evening meal, I do not want to come

home with lasagna noodles.

I'm building an analogy here but think about it: would you

ever go to a grocery store and ask an employee for some pasta, and just accept

the random type, size, brand, or package they gave you? Of course not. And yet,

when I look at most folks' portfolios, of all sizes and shapes, it seems like

most investors are just buying randomly the "noodles" someone hands them. I

know this isn't what happened; I know people spent time thinking about their

investment choices, but the result often looks like a random hodge-podge or

pasta bowl.

This reality is particularly important to acknowledge at the

beginning of a calendar year. Like it or not, most public companies, or anyone

that has shareholders or regulators, must worry about accounting. Most portfolio managers are worried about quarterly

(or even monthly) reporting requirements. I have been engaged in many

situations in which a portfolio manager would acknowledge that they have

positions that are sub-optimal, but they still hold on to them because the

accounting optics would not be great (for instance, it would result in

accounting for a realized loss). So, it remains—a piece of linguini among the

ziti.

As managers, none of us would ever want to act like that. We want better positions, better outcomes, and better returns…right?

I think we

would all say that. Our goal as managers should always be the

highest possible prospects for returns within acceptable risk parameters. That

seems so obvious when we think about it objectively, and yet the accounting,

regulatory, and reporting environments often leave us holding random, wrong

noodles long after the best "menu" has changed. I've been in hundreds

(thousands?) of meetings with portfolio managers and have yet to meet someone

that has said they intentionally want lower future returns.

This fits in perfectly with the themes I have been covering

over my last several posts. We all have and will make errors. It's just part of

this great game we are all playing called investing. A random, out-of-place

asset in your portfolio, like a random piece of pasta in the bowl I've been

describing, may have always been a mistake. Or it may be a left-over from

another time when it was the best thing on the menu, but no longer has a future

role.

As I have said many times before, sometimes unwinding these

situations is an opportunity. The ability to explain errors and describe

corrective measures enhances your credibility, and the ability to walk others

through why an asset already has performed and therefore has nothing more to

offer, can build understanding and confidence.

So, can I tie this back into my favorite homemade pasta tagliatelle? I think so.

Right now, we are being peppered with news stories of

inflation and the Fed raising rates. I personally happen to think we will be

seeing high inflation through all of 2022, but I might be wrong! Oil has been

shooting much higher. Rates seem to be heading higher, but we cannot fall into

the trap of thinking that we know what is going to happen. China is stumbling,

Russia is on the move, and there are tons of political risks out there that I

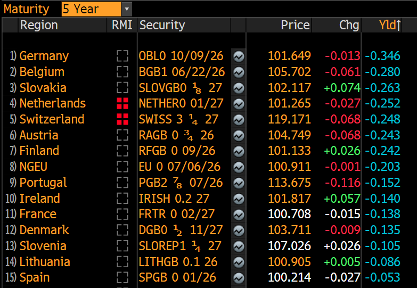

know I haven't even heard of. In most of Europe, 5-year rates are still

negative. If you look at this table, you will see 15 European countries with

negative rates out to the 5-year part of the yield curve (their 5-year yields

are in the rightmost column).

On my last post, linked

here, one of my predictions for 2022 was that Russia would invade Ukraine.

What would that do to rates? What would it mean for the stock market? So then, how

should a rational portfolio manager react to today's market conditions?

I think it's simple (although not easy), and this is the

same message I have been preaching for the last 24 months: we need to be

looking across multiple scenarios—over time. It's hard and it's messy, but bear

in mind that even if we are (or perhaps, because we are) subject to

incredible accounting and reporting consequences, the time to take corrective

actions is at the beginning of the year. Many of us have a very

complicated and messy bowl of noodles we call a portfolio. Is it tagliatelle,

spaghetti, or maybe a lasagna? I think (and this is my opinion) that if you

went to any superior or shareholder and told them a particular action could

improve their go-forward financial position, even if it caused some sort of

short-term accounting challenge, they would encourage you to pursue it.

Wouldn't you, in their shoes?

So, what's the action item? Review your noodles.

You may

have to take some action that makes you feel slightly uncomfortable, in the short

term, but which should, in any rational organization, raise your stature in the

long term. Doing the right thing is tough sometimes but bringing the right

noodle home saves you an extra trip to the grocery store!

Final, final thought: One of the inspirations for this post

was a recent plate of Tagliatelle alla Bolognese…beat it if you can!

Fill out the form below to subscribe to my weekly blog.

The information, analysis, guidance and opinions expressed herein are for general and educational purposes only and are not intended to constitute legal, tax, securities or investment advice or a recommended course of action in any given situation. Information obtained from third party resources are believed to be reliable but not guaranteed. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice.